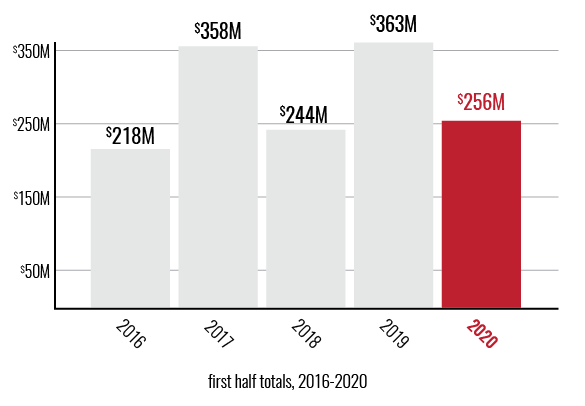

- Despite the tumultuous start to the year, early and growth stage companies in Medical Alley raised over $250 million, almost exactly the five-year average for the first half.

- Medical device companies in Medical Alley raised more than their counterparts anywhere else in the country.

- As the conversation around aging in place accelerates, Medical Alley is well-positioned to lead this revolution in healthcare delivery.

One of the dominant themes of 2020 so far is the tremendous amount of uncertainty present in nearly every segment of life. Is it safe to go visit relatives? Will the COVID-19 vaccine be finished before the holiday travel season? Which treatments are currently showing promise and which have fallen out of favor?

With all the turmoil affecting not just the economy but every part of society, a relatively normal first half for Medical Alley’s growth stage ecosystem is all the more remarkable. In total, 40 companies raised $256,406,357 in the first six months of the year, the third highest first half in the last five years. The $1.75 million median raise falls narrowly behind last year’s record $1.99 million as the second highest median raise for a first half in the last five years, indicative of a class of companies that took earlier stage rounds in previous years and have successfully grown and matured.

Medical Alley Device Companies Lead the Nation, Tackle Widening Array of Conditions

The story of the year so far — outside of the impact of COVID-19 and the economic downturn that has followed — has been the strength of the early and growth stage device sector here in Medical Alley. The vertical is responsible for over $213 million in raised funds this year, placing it ahead of traditional competitor clusters like San Francisco, San Diego, New York City, Boston, and Austin.¹

Leading the year’s device class so far is Conventus Orthopaedics, which raised $64.7 million in multiple tranches. They are followed by Histosonics ($40.7 million), Aria CV ($31.7 million), and Cardionomic ($15.8 million). These companies represent a wide swath of device subsectors, a trend that continues further down the raise total list: Of the 10 largest raises by a device company so far this year, nine seek to solve unique problems across seven different anatomical systems. Cardiology remains an area of particular expertise for the region, but orthopaedics and oncology are growing rapidly as well, as evidenced by sizable rounds in previous quarters for companies like Relievant Medsystems and Vyriad.

Medical Alley Advances the Future of Home Care

Research on the benefits of aging in place has increased dramatically recently and efforts to make that a reality have become all the more critical with the rapidly aging population putting strains on traditional healthcare providers. The additional risks for this population related to COVID-19 have set the benefits in even greater relief and instill renewed urgency in getting the right systems in place for our seniors.

Given this focus and timing, it is unsurprising to see both existing companies investigating how to turn the home into the primary site of care and a group of startups looking to disrupt the delivery of care to seniors. In the former category, Best Buy continues to make strides, connecting patients with their care team through both services and devices. Their partnership with TytoCare and acquisition of Critical Signal Technologies in 2019 were both indications that Best Buy was committed to transforming healthcare in the home and leading the rest of the field forward.

Representing the startup side is Lifesprk, which closed a $16.1 million Series A round in April to provide in-home care for seniors. While the home care nurse model has existed for decades, Lifesprk looks to integrate recent advancements in our understanding of the social determinants of health to provide the type of care that offers seniors more vitality, decreasing the cost of their care and potentially extending their lives.

As digital health tools become commonplace, using the home as the primary site of care will become easier, but the current generation of seniors doesn’t have the same level of digital literacy as subsequent generations will, which makes bridging that gap all the more critical. Companies that can blend innovative tools and methods, particularly with respect to remote patient monitoring, with the human element that is a critical part of care should find willing partners from nearly every sector of the healthcare industry.

M&A Update

One surprising change in the M&A market so far this year was the lack of disclosed values of deals; just one of the eight deals closed so far this year had a known purchase price — Altaris Capital Partners’ purchase of Kindeva Drug Delivery from 3M for $650 million — though Optum’s purchase of Tennessee-based NaviHealth was rumored to exceed $1 billion. Among the notable acquisitions of the year so far were Conventus Orthopaedics’ purchase of Flower Orthopedics, fueled by the year’s largest raise to date, and a pair of buys for Medtronic that expanded their capacities in robotic surgery and pain therapy.

Following an acquisition that appeared in the 2019 edition of this report, 3M’s $6.7 billion buy of Acelity, the Medical Alley giant looked to streamline their business, eventually electing to spin out their drug delivery unit. On May 1, that newly independent unit became Kindeva Drug Delivery — though 3M did retain 17% of the company. Kindeva will be a leader in, and an asset to, the rapidly growing Medical Alley biotech sector.

Looking Ahead

The inconsistent state of economic reopening makes predicting Q3 challenging at best; we know there will be headwinds, but the extent to which they will materially affect investment isn’t clear. Privately, investors have told the Medical Alley Association there is still an appetite for dealmaking particularly within digital health, but a lack of clarity regarding what changes will be made permanent with regard to reimbursement is making valuations variable and agreements slower moving.

The investment year to date has been far more normal than circumstances would suggest and Q3 is already off to a promising start. Healthcare has proven to be more durable than numerous other sectors — understandable in the midst of a pandemic — but make no mistake, the decades of work put in to build the Medical Alley early stage ecosystem is why when investors want to back companies working on the most innovative solutions to healthcare’s biggest problems, they look to The Global Epicenter of Health Innovation and Care™.

¹ via Crunchbase analysis of 2020 medical device raises in stated regions.